Payment innovation

EU’s Digital Markets Act: an opportunity for merchants to take back control of their payments

Businesses trading on Europe’s biggest app stores and e-commerce marketplaces will soon be free to select their own preferred payment service provider, thanks to a new European Union rulebook coming into force next spring.

The Digital Markets Act (DMA), which became law earlier this year and is now being implemented by the European Commission (EC), will unshackle merchants who currently have little choice but to accept the payment services offered to them by the world’s leading BigTech platforms.

In this blog, we unpack the objectives of this transformative piece of legislation and the initial group of platforms it will apply to. We outline the new obligations those platforms will have to comply with from March 2024. And we explore the huge opportunity these changes create for merchants seeking alternative, more cost-effective ways of accepting payments from their customers.

A new rulebook for European digital markets

How we live, work and interact with one another are all touched, in some way or another, by digital services. An ever-increasing share of overall economic activity takes place in digital ecosystems; whether buying and selling, we’re increasingly likely to do this online. It’s been estimated that the digital economy could account for almost a quarter of global GDP by the middle of this decade.

BigTech firms have emerged over the last 20 years as the preeminent players in this increasingly digital economy. They’ve redefined how, where and when people communicate and transact. Consumers have undoubtedly benefited immensely from the social networks, e-commerce marketplaces and related services they’ve built.

But EU policymakers have become increasingly uncomfortable with the prominent position these largely non-European companies now occupy. They fear that European businesses’ and consumers’ growing reliance on their services could stymie home-grown digital innovation and undermine free consumer choice.

To address these perceived risks, the EC has led an ambitious programme of digital reform over the last four years, resulting in new EU rules, rights and obligations for the biggest players in digital markets. The DMA is the centrepiece of this reform agenda.

This ambitious and wide-ranging piece of legislation aims to create a more level digital playing field in Europe through clear ‘rules of the game’ for digital platforms, so that lengthy antitrust investigations are no longer the only means for policymakers, businesses and consumers to tackle competition concerns.

What is a digital ‘gatekeeper’?

The DMA imposes a new set of obligations on large-scale companies that provide one or more ‘core platform services’ in the EU.

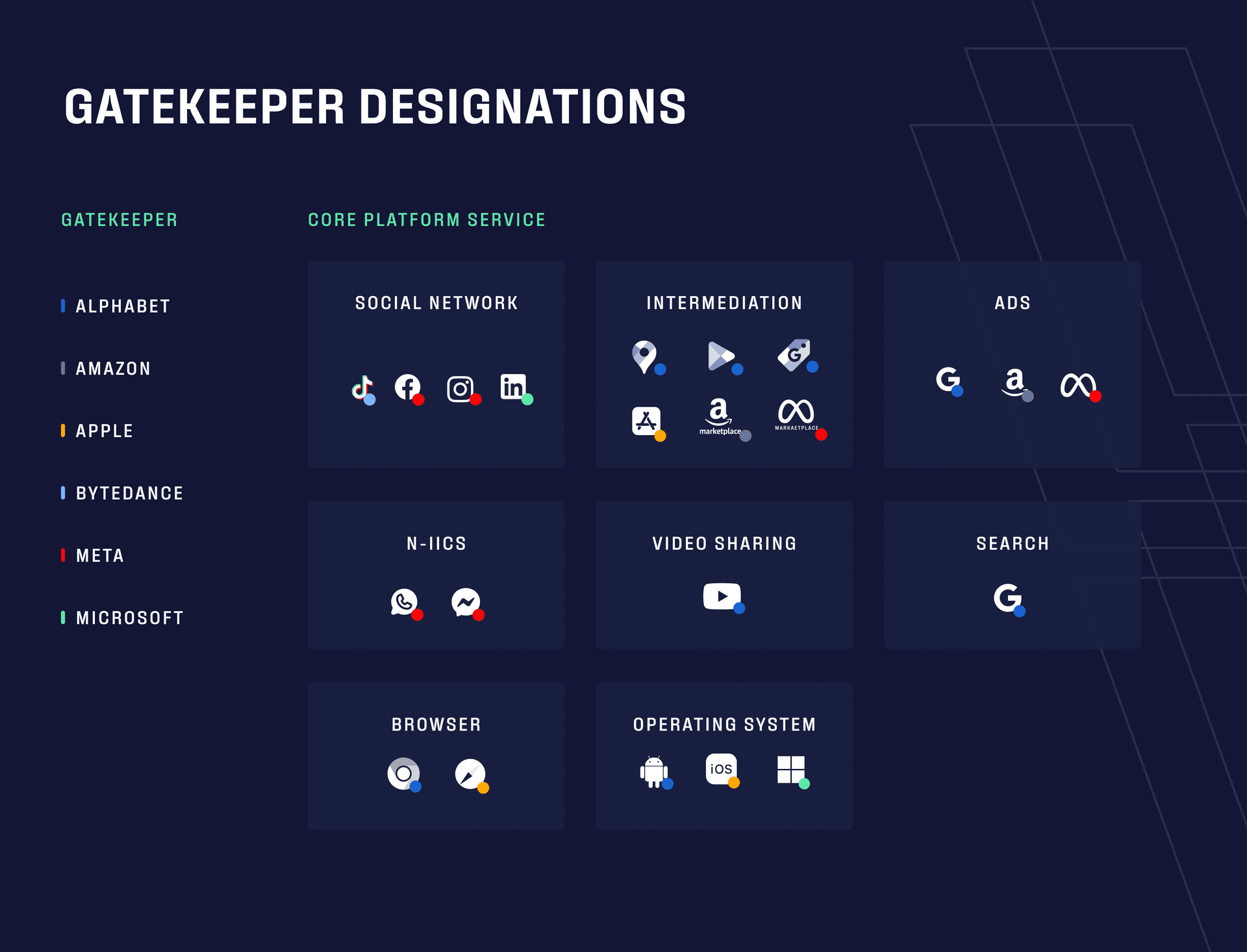

Ten core platform services are covered by the DMA. These include digital marketplaces, operating systems, digital messenger services, video sharing websites, online search engines and social networking services.

Companies that provide one or more of these services — and also meet the following three size-based criteria — are considered ‘gatekeepers’ under the legislation:

- Significant impact on the EU’s internal market – Annual EEA turnover of at least €7.5bn in each of the last three years, or an average market capitalisation of at least €75bn over the last financial year; and provision of their service in at least three EU countries

- Important gateway for business users to reach their end users – Over 45 million monthly active end users, and over 10,000 yearly active business users in the EU in the last year

- Occupy (or could in the future) an entrenched and durable market position – Presumed to be the case if the company met the second criterion in each of the last three years

Companies meeting these criteria are formally designated as gatekeepers by the EC, triggering a requirement to comply with a list of ‘do’s and don’ts’ contained in the DMA.

And it’s these obligations that create an opportunity for merchants to use alternative payment services to those they may currently be locked into by the gatekeeper company through which they reach their customers.

BigTech companies caught by the DMA’s noose

In September 2023, the EC formally designed six gatekeepers: Alphabet, Amazon, Apple, ByteDance, Meta and Microsoft. In total, 22 core platform services offered by these companies have been brought into the DMA’s scope. They are detailed below.

These six gatekeeper companies were given six months to comply with the DMA rules — which means they have to have come into line with the legislation by March 2024, and report on the solutions they’ve implemented to do so. Two of the above companies have legally challenged their designations.

A more open and innovative digital environment beckons

Gatekeepers will be encouraged by the DMA to behave in a more open way online – fairer for businesses and consumers, and more supportive of innovation – by complying with specific obligations contained in the legislation.

For example, their platform services will have to allow consumers to easily remove pre-installed apps, and to be able to install third-party apps or app stores. Gatekeepers will also be barred from using the data of their business users when competing with them on their own platforms, and prevented from ranking their own products or services in a more favourable manner.

Merchants will be given more freedom to contract with third-party service providers when selling through their core platform services. Gatekeepers will, for instance, have to allow business users to promote their offers and conclude contracts with their customers outside the gatekeeper's platform, and enable third-parties to interoperate with their own services.

And crucially from a payments perspective, the DMA bans gatekeepers from requiring app developers to use their own services, including payment systems, as a prerequisite to appear in their app stores. We dive into this in more detail below.

These are significant new obligations, and the EC is armed with equally significant regulatory sticks to ensure compliance. Any gatekeeper that fails to obey the rules faces a fine of up to 10% of their total worldwide turnover, rising to 20% for repeat offenders — and in some situations, they could be forced to sell businesses, or banned from making acquisitions.

Merchants will be able to shop around for payment services

Amongst other things, the DMA empowers businesses selling through a gatekeeper platform to choose their own payment service provider, rather than having to settle with the platform's own embedded offering.

As the EC itself says in its explainer on the legislation, 'gatekeepers will need to...allow developers to use alternative in-app payment systems'. This requirement is spelt out in Article 5 (7) of the DMA, which states:

"The gatekeeper shall not require end users to use, or business users to use, to offer, or to interoperate with, an identification service, a web browser engine or a payment service, or technical services that support the provision of payment services, such as payment systems for in-app purchases, of that gatekeeper in the context of services provided by the business users using that gatekeeper’s core platform services"

This provision opens up a world of new possibilities for businesses to optimise their checkout — and their operating costs — by selecting a payment service provider that better meets their specific needs. They no longer have to just make do.

For a long time, merchants have been crying out for faster, more secure and more cost-effective alternatives to the global card networks for accepting payments from their customers. In more recent years, they’ve been campaigning for the freedom to choose payment services that work better for them in the digital markets they serve.

Soon, thanks to the DMA, both will be in much closer reach for thousands of businesses across the EU.

An opportunity to harness the power of real-time payments

Alongside this new freedom for merchants to choose the payment service that best suits their needs, European lawmakers are overhauling laws to make account-to-account payments an even more attractive alternative for them.

In the run up to the DMA taking effect next spring, the EU will finalise legislation that will, in the next two years, make instant payments ubiquitous across the euro area. Legislators are also in the midst of upgrading the EU’s pioneering open banking rules. And building on this foundation, Europe’s open banking ecosystem has together designed a framework for new ‘premium’ open banking services, such as dynamic recurring payments.

In combination, these reforms will unlock a multitude of new use cases for open banking payments, spreading the associated benefits of instant settlement, bank-grade security and cost-effectiveness more broadly across Europe’s digital economy.

We firmly believe that real-time account-to-account payments will become the new normal – and that in time, real time will be the only time. The DMA will bring this a step closer for merchants.

More like this

Open banking

Industry deep dive: Exploring player behaviour trends in eGaming

We uncover the latest player habits shaping the eGaming landscape, and how open banking delivers on the demand for superior in-game payment processes.

Open banking

How much are card fees: A complete guide to processing costs

From interchange fees to scheme costs, we explore the full set of expenses that come with accepting card payments - and how they can be avoided through open banking.

Market insights

How PayTo compares to other payment methods in Australia

Explore the advantages of PayTo over other payment methods in Australia when it comes to fees, transaction speed, security, and user experience.